As an experienced mortgage adviser, I like to analyse things like home loan risks and maybe I do it more than most.

It appears to be that way anyway!

My name is Stuart Wills and I recently commented on a Facebook post to point out the risks of increasing the repayments if you have an ANZ home loan. It appeared that the person at the ANZ branch had not pointed out the risks of increasing the repayment, but also I was a bit disappointed to hear that a mortgage adviser didn’t either.

So let me explain what the issue is with ANZ home loan risks, and more importantly how to address that issue and minimise the risks to the borrower – the ANZ customer.

First, I will point out that I have over 25 years’ experience with mortgages, and over that time, I’ve seen a lot of changes in the industry, and we’ve gone through a lot of different economic cycles. My expectation is that the next 25 years, we will see the same.

We will see changes in the banking industry, and given technology, those changes could be a lot more than what we’ve seen in the past. And no doubt, we’re going to see changes in the marketplace with interest rates going up and down as they always have.

We also know that for most people, a mortgage is going to be a long-term financial commitment. When most people take out their mortgage, it is established over a 30-year loan term, and the intention is always to pay it off a lot sooner than that. But a lot sooner for most people will still be 15 to 20 years or more.

Therefore, a mortgage is a long-term financial commitment.

So given that we know that you will have a mortgage for some time, then in all likelihood, you will go through periods where interest rates are higher and periods where interest rates are lower. You will also go through times in your life where things are good and times in your life where things may not be so good and finances might be tight. Because of this, you want to ensure that you have a mortgage that gives you flexibility, not a mortgage that constrains you too much.

And this is where I have a problem with how some of the banks have structured their home loans.

A good home loan—any home loan—is going to be a major financial commitment but ideally you want a home loan that gives you the flexibility to pay it off faster when interest rates are low and you’re feeling financially okay, but then to be able to minimise your repayments in those times where interest rates spike to higher levels or when your personal circumstances mean you don’t have the surplus cash available.

That might seem quite logical, and many people believe that their mortgage does have that flexibility. They believe that the smiley face at the bank or the friendly mortgage broker has given them the right advice and is there to help them whenever needed. Logic says that they are paying their mortgage off faster, and that’s the right thing to do.

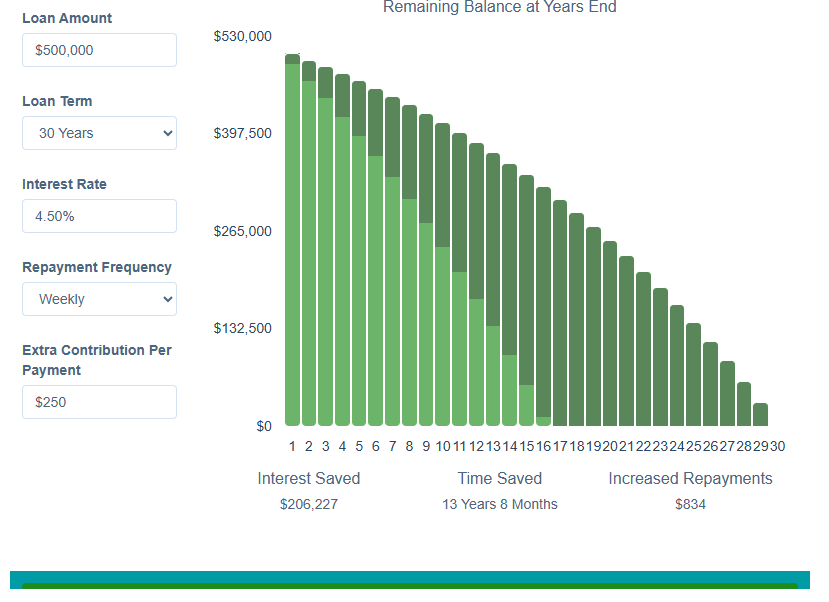

As mentioned, as a mortgage adviser, I like to help people pay their mortgages off faster and give them the advice they need so they don’t take on unnecessary risks that might see them get into financial trouble. Therefore, my point with the ANZ home loan is that they do allow you to pay the mortgage off faster. They even advertise and encourage you to pay the mortgage off faster (an extra $250 per week and/or lump sum of 5% per year) but what they fail to tell you is that when you do increase your repayments, you are locking yourself in to a shorter loan term.

Now let that sink in.

You are locking yourself in to a shorter loan term. What that means is your future repayments are then based on that shorter loan term. And so if interest rates increase (which we know they will one day)then your repayments will increase, and possibly increase so that they are unaffordable.

Let’s consider this: you have your mortgage of ‘say’ $500,000 locked in at 4.50% and you are feeling relatively comfortable financially, and so you increase your mortgage repayments by the maximum $250 per week that you’re allowed with ANZ. By doing that, you have reduced your loan term by over 13-years and on the face of it, it makes sense, and you’re happy to do that.

However, when your mortgage comes off fixed and interest rates have increased, you might be in trouble. You might find that your repayments jump up from what you were paying to an amount that you can no longer afford.

If the new interest rate was ‘say’ 7.00% then your mortgage repayments could jump from about $800 to over $1,300 per week. That’s an increase of over $500 per week!

Now, the bank might tell you that it’s no problem – you can come and see the bank, and they will extend your loan term out.

Initially that was their answer when I raised the issue; however, it’s important to understand that they have to assess and approve any increase to the loan term and that means that you’re at the mercy of the bank. Neither you nor the bank staff can know what they’re prepared to do at that time in the future when you’re going to ask them for help.

My question is, why would you put yourself in a position like that?

Therefore, what you need to do is look at the structure of your home loan. If you are going to increase your repayments on your ANZ home loan, then you should split off a portion of your lending and increase it only on that part of the loan. Don’t increase your repayments on the whole mortgage as that could put you into a very difficult situation in the future.

Know The Home Loan Risks

As mentioned, I am a mortgage advisor with a number of years’ experience, and I have had to mop up the mess that’s been left in some situations exactly like this.

If someone at the bank tells me it’s not a problem, I don’t believe them. That’s because I’ve seen the problems, and I’ve seen situations where bank customers have done what they thought was the right thing by increasing their repayments and paying their loans off faster, but got into situations where the bank refused to help.

And I’m not talking about 20 years ago – I’m talking about recent situations in the aftermath of COVID when interest rates spiked from around 3.00% to closer to 7.00% and we saw a lot of people get into financial difficulty. That’s the reality of it, and that’s why I’m passionate about telling people not only the good things about home loans, but raising the real home loan risks with them too.

IMPORTANT NOTE:

Kiwi Edition is provides simplified news and views on all things finance related in New Zealand.

On a final note, this is not purposefully directed at any bank, at any bank staff or mortgage advisers – it’s a warning to everyone that has a home loan that it is up to you to get the best advise and know how your home loan works, and then maximise what you do with that home loan and within the risk tolerances that you have.

As a mortgage adviser I have dealt with many banks and lenders over the years. Some are still here operating today and others have vanished. In this article I am pointing out a risk with the home loan offered by ANZ and I have also discussed this with my managers at ANZ so they are aware of the issue too. We still use ANZ as a lender and they , but it’s always been extremely important to get good advice and make sure that you minimise the home loan risks while at the same time making sure that you do pay off your mortgage faster.

{kind=link}